The economic effects from COVID-19 are on track to send state government into severe fiscal trouble. As such, a consensus group of state forecasters reduced tax revenue estimates, anticipating a COVID economic shock. However, estimates from national forecasters cast serious doubt on how realistic Kansas forecasters are. There’s considerable evidence Kansas consensus group vastly underestimated the COVID-19 shock by (at least) hundreds of millions of dollars.

On April 20th, economists and analysts from the KU, Kansas State, WSU, and state agencies met to predict the impact the economic hit COVID-19 will have on state coffers. Known as the Consensus Revenue Estimating Group or CRE, they meet every April and November to guess state tax revenue. The CRE guessed Kansas total receipts would drop roughly $540 million from 2019 to 2020. In 2021, the state coffers would see a rebound of $405 million. While these estimates are massive by themselves, are they in line with national economic expectations? We answer this question.

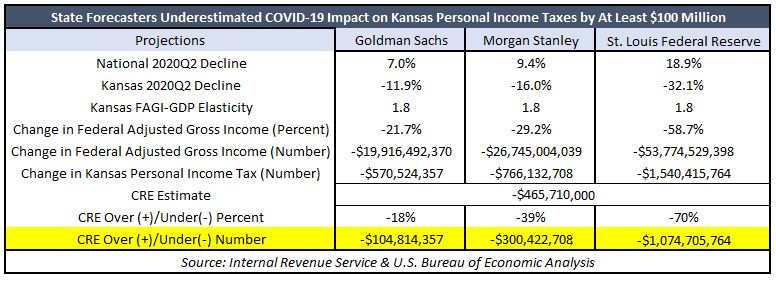

Goldman Sachs, Morgan Stanley, and St. Louis Fed Estimates

The economic fallout from the COVID-19 virus will likely be the sharpest downturn in recent national history. Consensus for the U.S. second quarter of 2020 economic impact ranges from Goldman Sachs with a -7% hit, to Morgan Stanley’s -9.4% impact, to the Federal Reserve Bank of St. Louis’s predicting a whopping 18.9% contraction. We translated each of these national impacts to a Kansas fiscal impact and compared it to the CRE 2020 estimate. See the Appendix for our methodology.

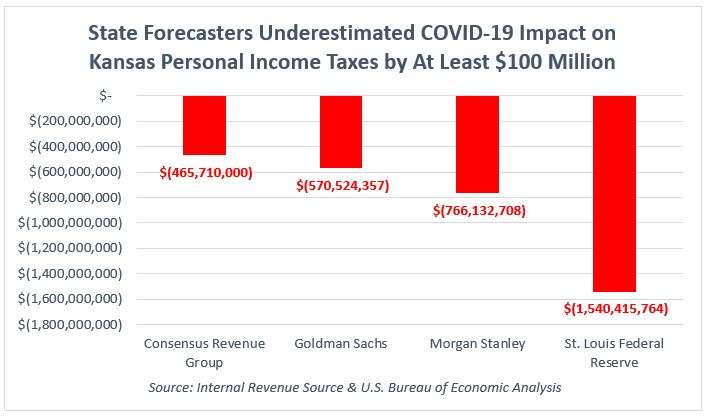

The two charts above compare the CRE’s estimate on Kansas’ total receipts and personal income taxes to national forecasters. The Consensus group’s total receipts estimate is less than half of the rosiest expectation from national forecasters (Goldman Sachs). If the worst-case scenario (St. Louis Fed) is real, then state forecasters would have prepared Kansas for less than one-fifth of the COVID-19 fiscal impact.

The two charts above compare the CRE’s estimate on Kansas’ total receipts and personal income taxes to national forecasters. The Consensus group’s total receipts estimate is less than half of the rosiest expectation from national forecasters (Goldman Sachs). If the worst-case scenario (St. Louis Fed) is real, then state forecasters would have prepared Kansas for less than one-fifth of the COVID-19 fiscal impact.

The following chart shows the same comparison but for Kansas’s largest tax revenue source, personal income taxes. The CRE’s estimate for personal income taxes is roughly 20% lower than the rosiest expectation from national forecasters. If the worst-case scenario is realized instead, state lawmakers might find trouble covering an additional billion-dollar gap from personal income taxes alone.

CRE’s Tax Impact Also Falls Short From Moody’s Projections

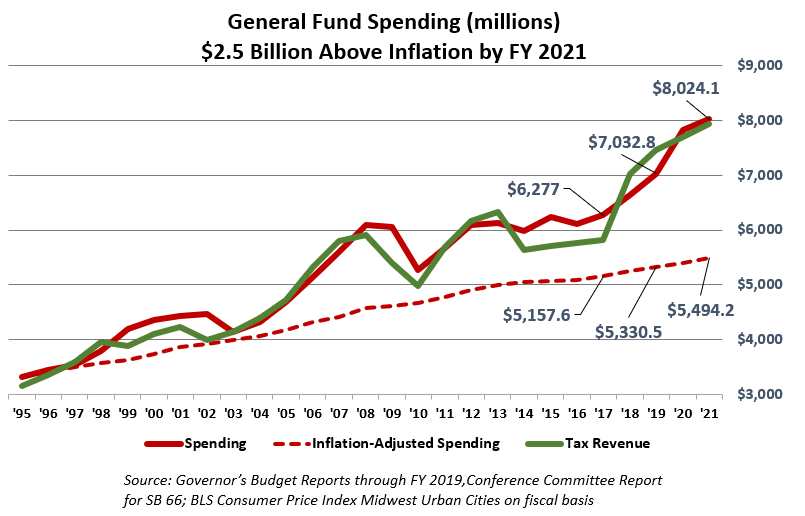

The estimates from Goldman Sachs, Morgan Stanley, and the St. Louis Fed for the Kansas economy fall in line with Moody’s Analytics Kansas estimation of the COVID-19 impact. Moody’s “Moderate Stress Scenario” estimated a $1.4 billion hit for Kansas in 2020. Their “Severe Stress Scenario” predicted a $1.9 billion impact. Usually, under an economic downturn, states can rely on their ending balances to cover any near-term shortfalls. However, Moody’s reports Kansas has no rainy-day fund as of Fall 2019. Consider the fact the state spent a record $8 billion, which is $2.5 billion above inflation since 1995. Kansas is in dire straits.

The estimates from Goldman Sachs, Morgan Stanley, and the St. Louis Fed for the Kansas economy fall in line with Moody’s Analytics Kansas estimation of the COVID-19 impact. Moody’s “Moderate Stress Scenario” estimated a $1.4 billion hit for Kansas in 2020. Their “Severe Stress Scenario” predicted a $1.9 billion impact. Usually, under an economic downturn, states can rely on their ending balances to cover any near-term shortfalls. However, Moody’s reports Kansas has no rainy-day fund as of Fall 2019. Consider the fact the state spent a record $8 billion, which is $2.5 billion above inflation since 1995. Kansas is in dire straits.

The CRE is not in line with the national consensus of the COVID-19 economic impacts. However, in Part 1 of our CRE analysis, we show the CRE has a history of making bad predictions. Let’s not forget, the CRE underestimated the most massive tax increase in state history by half a billion dollars. Moreover, they missed income tax projections by, on average, 10% between 2001 and 2016. Despite CRE’s acknowledgment that the Kansas COVID-19 economic shock will be greater than the Great Recession, state forecasters think the shock immediately disappears by 2021.

However, there’s a solution for policymakers irrespective of the predictions of the CRE. Within our Post-COVID recovery plan, we outline tools policymakers can use regardless of how significant the COVID-19 impact will be. The state can eliminate discretionary spending in part by enforcing Performance-Based Budgeting. Policymakers can eliminate vacant positions, and it can focus on growing its rainy-day fund. Finally, whenever Kansas policymakers decide to tackle the budget – in a veto session, through gubernatorial recissions, or in 2021 – they should view CRE predictions with skepticism. Otherwise, they risk turning a blind eye to national economic expectations and a history of inaccurate state budget predictions.

Appendix

To translate U.S. economic decline to a Kansas performance, we calculated Kansas to U.S. ratio of economic growth during the Great Recession and found a value of 1.7 (for every 1% change in U.S. GDP, Kansas GDP changes 1.7%). This ratio allowed us to compute Kansas 2nd quarter declines of 11.9% to 16% to 32.1%.

From there, we measured the elasticity, or the correlation between Kansas GDP and tax revenues from 2002-2017 and found a value of 1.6 (for every 1% change in Kansas real GDP, total receipts change by 1.6%). Taking the elasticity multiplied by the Kansas economic decline got us the percent change in total receipts, which measured a 2020-dollar change of at least $1.3 billion.

For personal income tax collections, we calculated the elasticity between Kansas GDP and Federal Adjusted Gross Income (FAGI), which stands as a base for personal income tax collections. This is because calculating personal income tax collections using income tax revenues would capture both changes in economic activity as well as changes in state tax policy.