The heavy burden of high property taxes is taking a toll on Kansans. But, there are solutions. Our local governments should address this crisis with a sense of urgency and stop the practice of backdoor tactics that raise property taxes without a vote.

It’s time for transparency and accountability. Here are the top five things homeowners need to know about property taxes in Kansas.

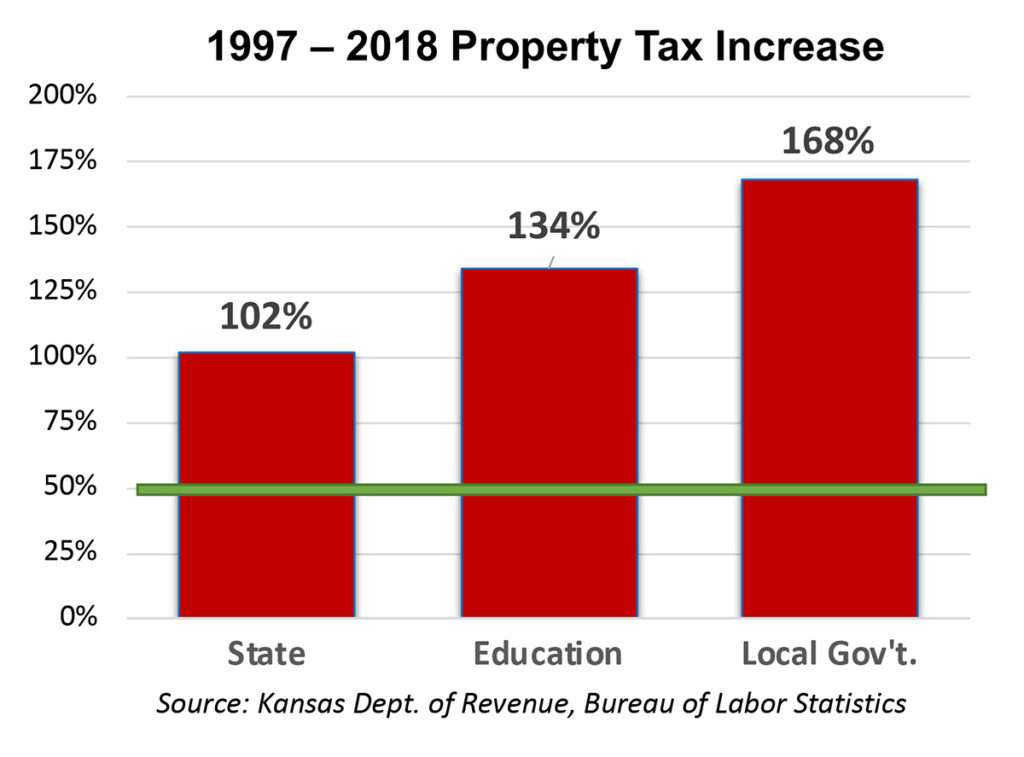

1. City and county property tax jumped 168% between 1997 and 2018

Property tax increased by 151% between 1997 and 2018, or more than three times the inflation rate of 50%. Property tax for local government (cities, counties, townships, etc.) totaled $2.7 billion in 2018 or about 54% of all property tax. Local government also imposed the largest increase, averaging 168%.

Public schools and community colleges account for about 45% of the total, taking in $2.2 billion, and only 1% of property tax goes for the operation of state government.

Additional Resources:

Local government has the biggest share of $3 billion property tax hike

Local government property tax data shows opportunity for savings

County spending patterns show room to cut

County graphs showing changes in property tax, inflation, mill rate, and population

City graphs showing changes in property tax, inflation, mill rate, and population

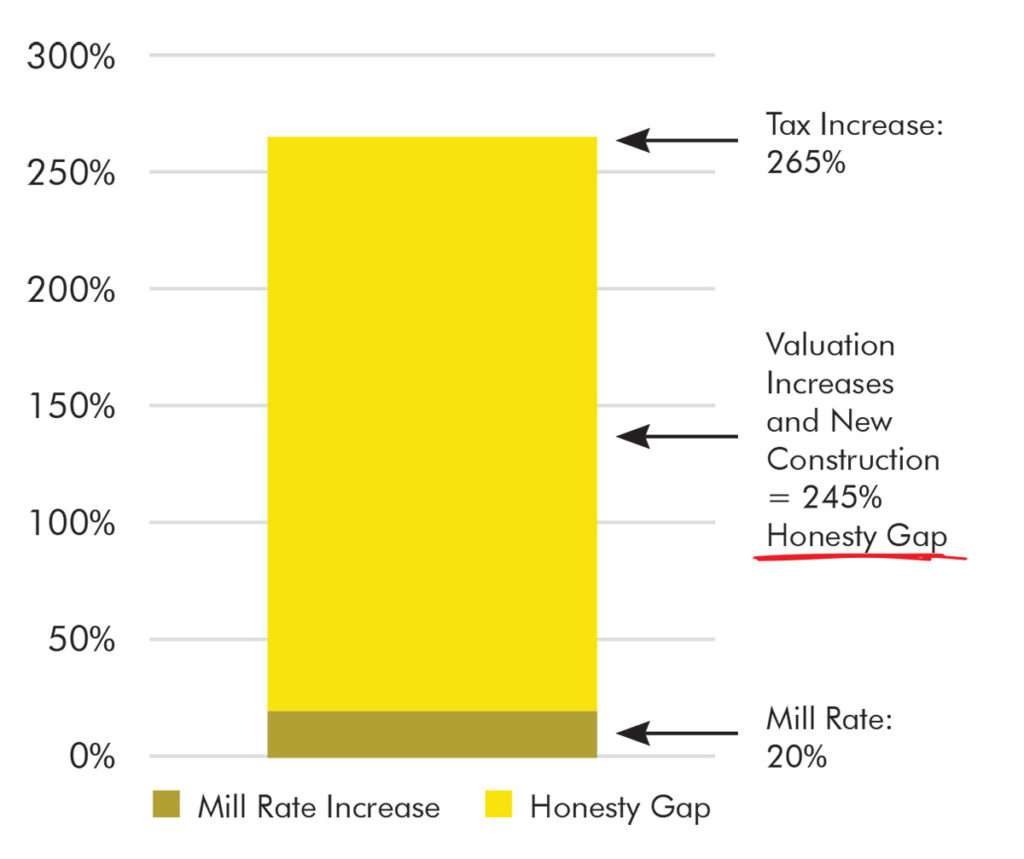

2. The Property Tax Honesty Gap

Some city and county officials say they’re ‘holding the line’ on property taxes, but voters are fully aware that property tax has been rapidly increasing because of valuation changes.

This chart shows Riley County increased property tax by 265% between 1997 and 2018, according to the Kansas Department of Revenue.

And yet the mill rate only went up 22%. That huge, 245-point difference between the actual tax increase and the change in the mill rate has created an honesty gap in taxpayers’ minds.

Mitchell County has the largest honesty gap among counties. Property tax for county operations jumped 402% while the mill rate increased by 120%, creating a 282% honesty gap.

Additional Resources

Property tax hikes are proof of an honesty gap

3. Legislation to close the honesty gap

Senate Bill 294, which is being discussed in the Kansas Senate currently, is modeled after the Utah legislation that has successfully reduced property tax rates. It simply requires city and county elected officials to vote on the entire property tax increase.

SB 294 doesn’t limit spending and elected officials don’t have to get public approval. They just have to vote on the entire tax increase they impose each year.

Once a city or county gets new valuation totals each year, a ‘Certified Rate’ is calculated to produce the same property tax revenue as the prior year based on the new valuations. Elected officials must notify taxpayers of their intent to increase the Certified Rate and hold a public meeting where people can comment. Then they have to vote to increase the Certified Rate, which means they are voting on the total tax increase.

The effective tax rate in Utah declined by 7.5% between 2000 and 2018, but the effective tax rate in Kansas increased by more than 22%.

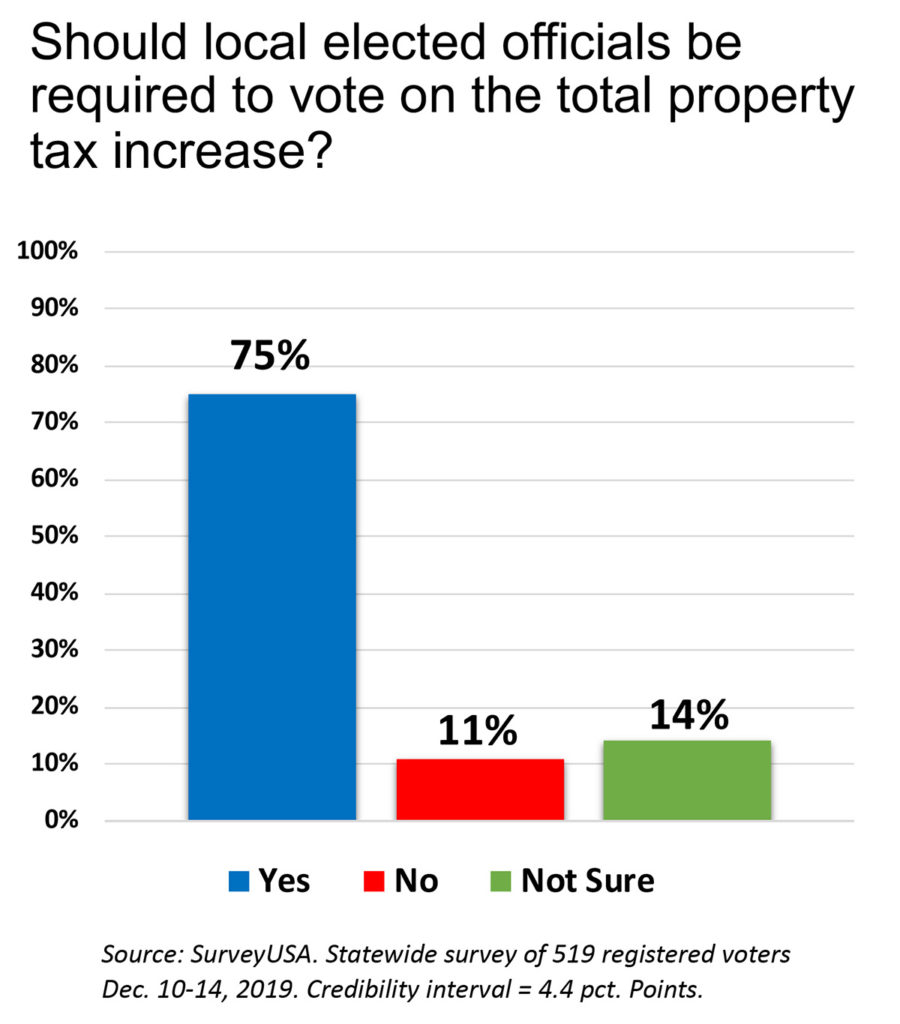

Cities and counties oppose SB 294 but voters overwhelmingly support this idea. A December 2019 public opinion survey conducted by SurveyUSA on our behalf asked whether local elected officials should be required to vote on the total property tax increase. 75% said ‘yes,’ and only 11% said ‘no’.

Cities and counties oppose SB 294 but voters overwhelmingly support this idea. A December 2019 public opinion survey conducted by SurveyUSA on our behalf asked whether local elected officials should be required to vote on the total property tax increase. 75% said ‘yes,’ and only 11% said ‘no’.

Support crosses all ideological and geographical lines. 73% of self-described liberals and moderates and 80% of conservates favor the change. Geographic support across the four regions (Western, Eastern, Wichita area, and Kansas City area) ranges from 72% to 78%.

Additional Resource

Link to complete survey results and methodology

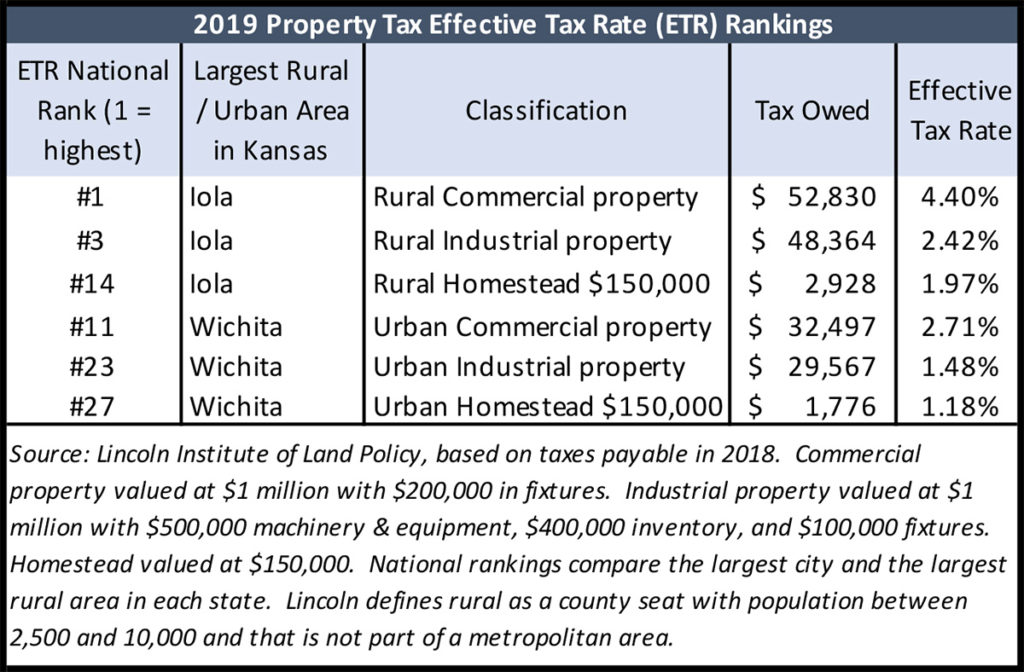

4. Kansas has the highest rural property tax in the nation

TheLincoln Institute of Land Policy’s 2019 50-State Property Tax Comparison Study shows Kansas is very uncompetitive on effective property tax rates. The effective tax rate (ETR) is the property tax paid as a percentage of assessed valuation.

Kansas’ rural rankings, comparing the largest county seats in non-metropolitan areas with a population between 2,500 and 10,000, are among the worst in the nation. Iola represents Kansas and has:

- — the #1 highest ETR on commercial property

- — the 3rdhighest ETR on industrial property

- — the 14th highest ETR on residential property valued at $150,000

Comparing the largest city in each state, Kansas has:

- — the 11thhighest ETR on commercial property

- — the 23rdhighest ETR on industrial property

- — the 25th highest ETR on residential property valued at $150,000

Property tax is an especially large barrier to economic growth in rural areas. The 4.4% effective tax rate on commercial property in Kansas is more than double the rate in Missouri and Nebraska and more than four times the ETR in Oklahoma.

Additional Resources

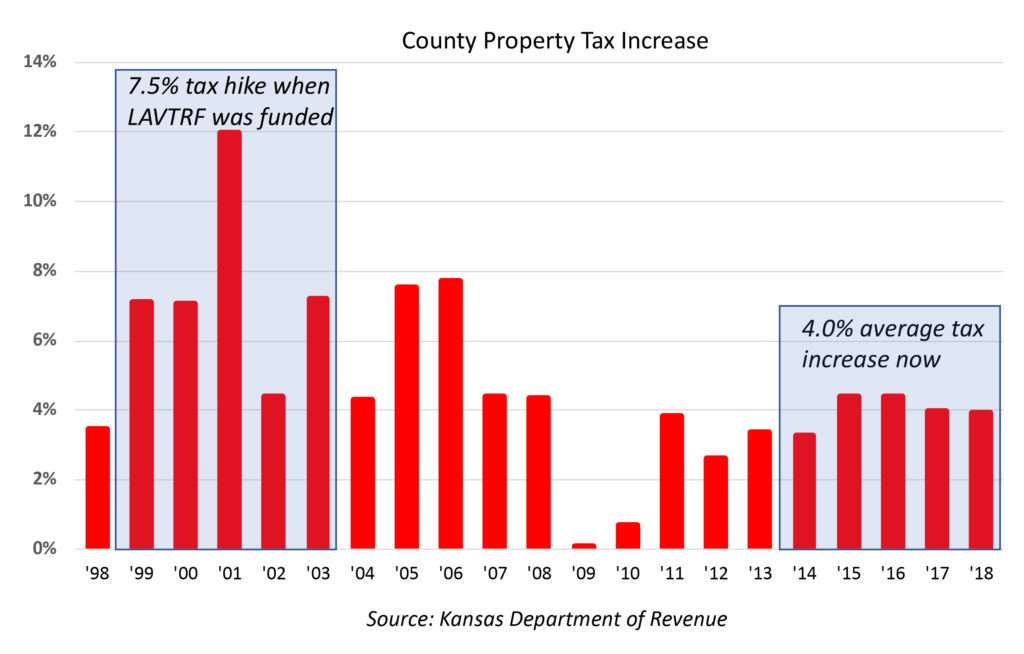

5. Kelly’s LAVTR property tax relief plan doesn’t work

Governor Kelly’s Tax Council members propose resurrecting the Local Ad Valorem Tax Reduction (LAVTR) program as their solution to high property taxes, saying “…local governments would once again have a strong tool to begin lowering local property taxes.” But that program didn’t work the last time, and it won’t provide tax relief now.

LAVTR was last funded in 2003. County property taxes increased by an average of 7.5% during LAVTR’s last five years; without LAVTR, county property taxes ‘only’ averaged a 4% annual increase over the five years ended in 2018.

There is no enforcement mechanism in LAVTR. In other words, cities and counties don’t have to prove they reduced property tax or even hold property tax flat. But even if it produced dollar-for-dollar local property tax reductions, the program merely leads to higher state sales and income taxes.

Kansas is already facing long-term budget deficits, so giving state money to cities and counties only increases the deficit and puts more pressure on sales and income tax increases.